|

||

| Sulphuric Acid on the WebTM | Technical Manual | DKL Engineering, Inc. |

Knowledge for the

Sulphuric Acid Industry

![]()

Sulphuric Acid on the Web

Introduction

General

Equipment Suppliers

Contractor

Instrumentation

Industry News

Maintenance

Acid

Traders

Organizations

Fabricators

Conferences

Used

Plants

Intellectual

Propoerty

Acid

Plant Database

Market

Information

Library

Technical Manual

Introduction

General

Definitions

Instrumentation

Plant Safety

Metallurgial

Processes

Metallurgical

Sulphur Burning

Acid Regeneration

Lead Chamber

Technology

Gas Cleaning

Contact

Strong Acid

Acid Storage

Loading/Unloading

Transportation

Sulphur

Systems

Liquid SO2

Boiler Feed Water

Steam Systems

Cooling Water

Effluent Treatment

Utilities

Construction

Maintenance

Inspection

Analytical Procedures

Materials of Construction

Corrosion

Properties

Vendor Data

DKL Engineering, Inc.

Handbook of Sulphuric Acid Manufacturing

Order

Form

Preface

Contents

Feedback

Sulphuric Acid

Decolourization

Order Form

Preface

Table of Contents

Process Engineering Data Sheets - PEDS

Order

Form

Table of Contents

Introduction

Bibliography of Sulphuric Acid Technology

Order Form

Preface

Contents

Market and Cost Information

October 11, 2010

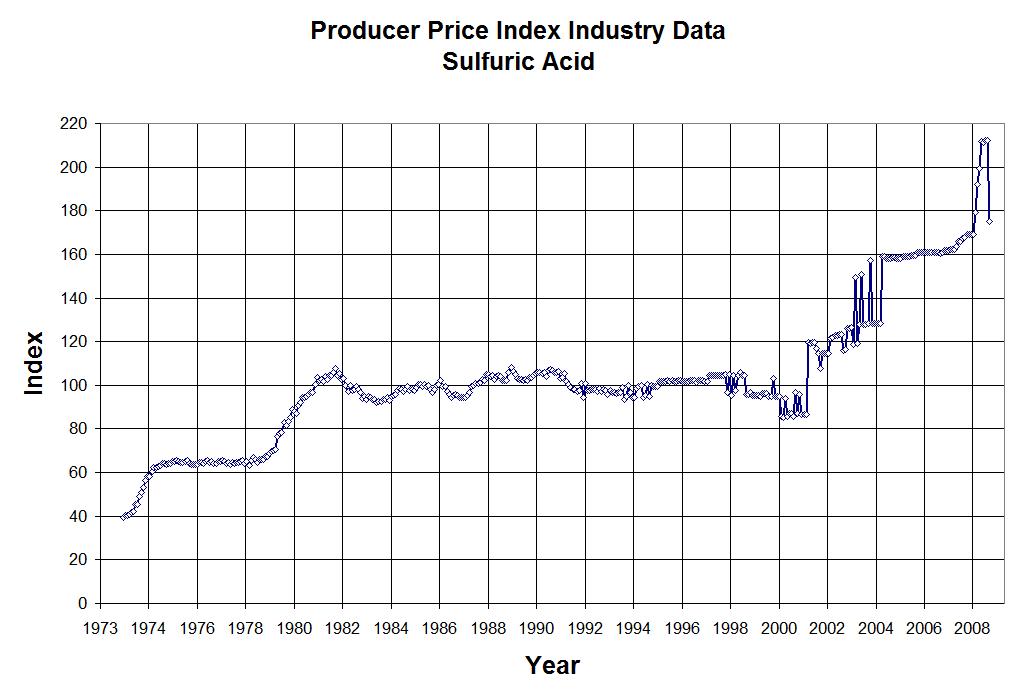

| U.S. Department of Labour Bureau of Labour Statistics Producer Price Index - Industry Data 325188 - All Other Basic Inorganic Chemical Manufaturing 3251883251881 - Sulfuric Acid |

|

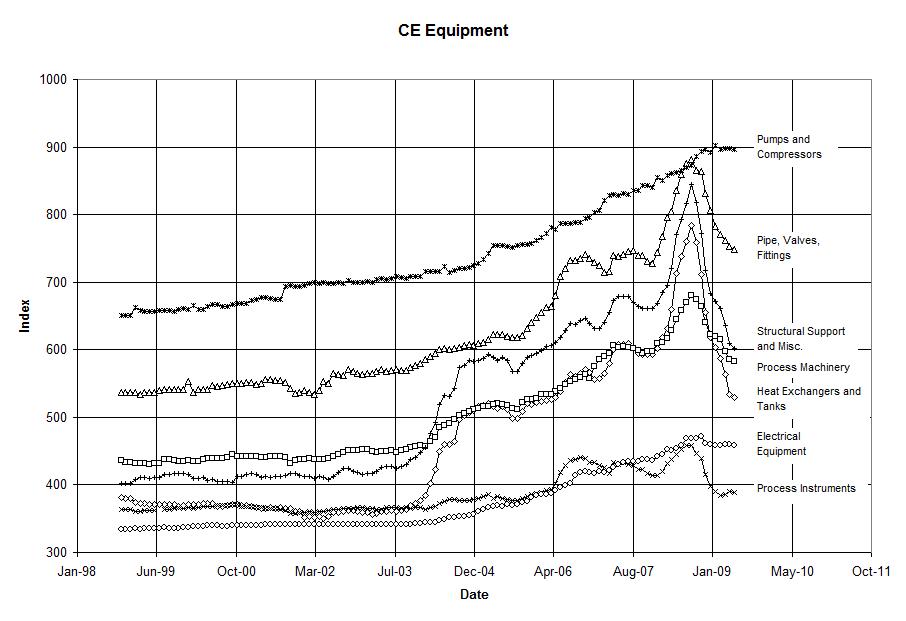

| Chemical Engineering Equipment Indices |

|

| Commodity

Prices (1 and 5 years) (October 11, 2010) www.kitcometals.com |

|

| Copper |   |

| Nickel |   |

| Lead |

|

| Zinc |

|

October 11, 2010 - Approximately 71425 MT of Chemicals is expected at Kandla and Dahej in the vessels Al Jubail, Bow Favour, Chem Hydra, Acacia, Chemroute Sun, Stolt Megami, Jo Sypress, Maritime Vanessa, Chem Hydra and Arabian Orchid.13453 MT of Liquid Ammonia will reach the port Mourmugao and Vizag in the vessel Al Marona and Gas Columbia.1007 MT of Mono Ethylene Glycol is expected at the port Chennai in the vessel Southern Unicorn.29500 MT of Phosphoric Acid is expected in the vessel Stolt Vestland at the port Kandla. 7168 MT of Soda Ash will reach the port Chennai in the vessel New Legend Harvest. 10000 MT of Sulphuric Acid will reach the port Vizag in the vessel Sun Bridge and 4202 MT of Vinyl Chloride Monomer is expected at the port Tuticorin in the vessel Catterick.

Oversupply of sulphur a challenge for

producers

MEED, Issue No. 27 2 – 8 July 8, 2010 - The

oversupply of sulphur is a key concern for the region as it looks to exploit

more sour oil and gas fields

June 17, 2010 - New Delhi, India - The Centre's decision to decontrol prices of all non-urea fertilisers simultaneous with the grant of a fixed nutrient-based subsidy (NBS) on individual products seems to paying off. The significant decline in global prices of most fertilisers and their intermediates in recent months has meant the Centre is under no compulsion now to raise subsidy payable to companies. And the latter have no apparent grounds to hike maximum retail prices (MRP) charged to farmers even in a decontrolled environment. In other words, contrary to earlier fears of decontrol leading to substantially higher farmgate prices or an expanded subsidy bill for the Centre, a bearish international market has ensured there is no pressure on either front at least for now.

Raw materials - Currently, urea of West Asia origin is quoting at $235 a tonne free-on-board (f.o.b.), as against $315-320 just three months ago. Inclusive of freight of around $12, the landed price at Indian ports would be hardly $247 a tonne. Likewise, prices of ammonia and sulphur – both used for manufacture of di-ammonium phosphate (DAP) – have eased considerably. Since mid-March, ammonia has dropped from $380 to $300 a tonne (f.o.b. West Asia), with landed prices here now at around $330 a tonne. Sulphur prices, which had touched $200 a tonne (cost & freight India) in March, have since slid to $120 or thereabouts.

Fixing subsidy - The Centre had, on March 16, fixed the per kg NBS rates at Rs 23.227 for nitrogen (N), Rs 26.276 for phosphorous (P), Rs 24.487 for potash (K) and Rs 1.784 for sulphur (S). These rates formed the basis for fixing the subsidy on individual fertilisers. For example, one tonne of DAP contains 180 kg of N and 460 kg of P. The subsidy payable to its manufacturers/importers, then, came to Rs 16,268 a tonne, while working out to Rs 10,133 for a tonne of ‘20:20:0:13' NPKS complex fertiliser. For arriving at the per kg NBS rates, the Centre had benchmarked them to import parity prices (IPP) of urea (for N), DAP (for P), muriate of potash (for K) and sulphur (for S), which were taken at $310, $500, $370 and $190 a tonne at Rs 46-to-the-dollar.

MRP hike unlikely - But with current landed prices – at $247-248 for urea, $470-475 for DAP and $120 for sulphur – actually ruling below the assumed IPPs, the Centre has two options. The first one would be to reset the unit NBS rates to reflect the lower import prices and, thereby, reduce the subsidy payable to manufacturers/ importers. The second option would be to force companies to slash farmgate prices, though this is theoretically inconsistent with a decontrolled regime. “They are unlike to do either immediately. What is more likely is that the industry would be informally directed not to raise MRPs in the coming rabi season, just as they were asked to cooperate and keep price increases within limits for this kharif,” sources pointed out. In fact, for the ongoing kharif season, companies had given undertaking that they would not raise the MRP of any non-urea fertiliser beyond Rs 30-35 a bag. Accordingly, DAP is now selling at a uniform Rs 9,950 a tonne (excluding local taxes), against Rs 9,350 prior to April 1, when prices were ‘decontrolled'. Moreover, companies have been made to clearly print the MRP along with the applicable subsidy on every bag of fertiliser they sell, with any sale above the printed rate punishable under the Essential Commodities Act. “The Centre's sole concern is that decontrol should not have any adverse political fallout. The decline in global prices is welcome to that extent,” the sources added.

Copper concentrate

market in deficit for 3 years - Freeport

June 12, 2010 - Bloomberg cited Mr Javier

Targhetta senior VP of marketing and sales of Freeport McMoRan Copper & Gold

Inc’s as saying that the copper concentrate market will have a shortfall for 3

years after miners delayed projects because of lower prices. Mr Targhetta

said that the deficit will be between 500,000 tonnes and 1 million tonnes this

year. He said that the concentrate market will remain tight over the next 3

years or even longer. Concentrate is the raw material from which copper is

produced. Barclays Capital said that mining companies delayed or scrapped

new projects after copper prices plunged a record 54% in London in 2008,

crimping future supply. Global mine production fell 0.1% last year. The refined

market is expected to show a deficit of 155,000 tonnes this year after a surplus

of 567,000 tonnes in 2009. Mr Targhetta said at the event, organized

by the GDMB Society for Mining, Metallurgy, Resource and Environmental

Technology with Hamburg based Aurubis AG that the shortfall in mined output will

keep the fees that mining companies pay smelters to turn ore into metal under

pressure for a long time. He said that smelters have received increased

supplies of scrap copper and have benefited from higher prices for sulfuric

acid, the largest by product from the smelting process. Mr Targhetta said

that scrap is helping smelters in China and also outside China. This year

Atlantic Copper’s plant in Huelva, Spain, will produce 20,000 tonnes of copper

from scrap up from 7,000 tonnes last year. He said that Atlantic Copper,

based in Madrid, produces about 1 million tonnes of sulfuric acid per year. This

year the company expects to produce 278,000 tonnes of copper anodes usually

refined into a finished form of metal known as cathode. That’s 8,000 tonnes more

than last year. Production of cathodes will reach 262,000 tonnes this year up

from 257,000 tonnes. He added that production will be lower next year as the

plant is scheduled to be closed for about 20 days for maintenance work.

Sulphuric Acid Prices

April 18, 2010 - Prices of sulphuric acid, a copper smelting by-product, have risen by half in China over the month, keeping operating rates high despite low copper treatment and refining charges (TC/RCs). Sulphuric acid prices have risen to touch 600 yuan ($89) per tonne, from an average of 400 yuan a month ago, delegates at the 2010 Beijing copper summit held by China Nonferrous Metals Industry Assn (CNIA) told MB. "Average prices could be around 500-600 yuan per tonne, thanks to rising demand for fertilizer".

Sulphuric acid prices held down by excess supply

April 7, 2010 - Purchasing of sulphuric acid has undergone a "dramatic turnaround" so far this year, according to CRU International, which says "rising demand is evident from the industrial sector, the phosphate fertilizer industry and copper leaching operations." However, inventories still are well in excess of renewed demand. So, near-term prices should stay around the $144/ton average of the first quarter and not approach the $200/ton average of 2009, according to the CRU report presented at this week's World Copper Conference in Santiago, Chile. While there is some tightness in the U.S. acid market, ICISpricing.com says production rates were slightly improved from a month ago. So, there is quite some debate whether spot prices will rise in the second quarter back to $150-$200, as sought by producers. Another issue is that phosphate fertilizer prices have begun to weaken, "undermining sentiment in the sulphuric acid market," says CRU. "It is too early to say whether the price boom-that brought U.S. market prices up from an average $107/ton in October and November-has come to an end, but market activity is very thin and there are growing indications that further increases may not be sustainable." The analysis suggests that supply of sulphuric acid is forecast to remain tight. So, drop in prices is unlikely for the next few months. However, the peak application season for phosphate fertilizers is almost over, and stocks of sulphuric acid are expected to gradually increase over the summer. "For this reason, the second half of the year will probably see prices coming down for both products," CRU forecasts. In another analysis of the world fertilizer market, TD Bank analysts also are cautious about offshore demand due to recent weakness in global crop prices, "which may limit the global demand fertilizer rebound volume and/or price gains." Source www.purchasing.com

Sulfuric Acid Goes From Worthless to

‘Crazy,’ Boosts Mine Costs

March 8, 2010 - The value of

sulfuric acid, used to dissolve metal ore and produce fertilizer, has gone from

worthless to “crazy” this year, increasing costs for mining companies,

London-based researcher CRU Group said. “It all changed very

quickly,” Joanne Peacock, an analyst at CRU, said in an interview in London

today. “Fertilizer demand was suddenly much stronger than expected.”

Rebounding market rates for the acid, a byproduct of copper processing, to more

than $100 a metric ton may help smelters of the metal to boost output as they

can profit from the sale of the residue. Stockholm-based Boliden AB was among

operators that previously cited the slump in prices as part of the reason for

curbing output. Miners, though, face rising costs, Peacock said. Demand

from fertilizer makers, normally about half of world sulfuric acid consumption,

has risen as higher prices for their products prompted companies to rebuild

stocks, Peacock said. “It’s all gone crazy,” she wrote in a separate e-mail

today. Supply from metal smelters, oil refineries and burning elemental

sulfur couldn’t keep up, she said. “The availability of sulfur has been

much lower than expected,” Peacock said. “The refineries haven’t been able to

increase their operating rates to full capacity yet because the U.S. consumer is

not buying as much diesel and gas.” U.S. oil refineries operated at 81.9

percent capacity in the week ended Feb. 26, according to the latest data from

the U.S. Energy Department released March 3. This time last year it was 83.14

percent and in 2008 output was 85.19 percent.

Surging market prices for acid will probably be

temporary as demand dies down, Peacock said. “I still see the underlying demand

picture as fundamentally weak and this situation may not last beyond the first

half of this year,” she said. Fertilizer demand fell to its weakest in

five years in 2009 as economic crisis and the credit crunch hurt farmers,

according to CRU. Annual contract prices for this year fell to about $30- $60 a

ton, from $110-$140 in 2009, Peacock said in December. Sulfuric acid

demand, typically about 200 million tons a year, will probably increase from

2009, though is unlikely to reach levels before the economic crisis in 2008, she

said.

China fertilizer Market

March 2010 -

In 2009, under the "positive fiscal, easy monetary" policy, the government has

implemented a large-scale economic stimulus plan, substantially lower interest

rates, take various measures to boost domestic demand and encourage exports. The

slowing down momentum of China's macroeconomic growth has been effectively

contained, and resumed an increase of over 8% compared the same period last year

in the second of 2009. As for external economies, the global economic recession

caused by the international financial crisis also has a certain degree of

recovery, the negative impact on China's economy began to be weakened.

In this context, China's fertilizer industry trends improved in the first half

of 2009. Since the beginning of the third quarter of 2008, weak domestic

consumption, stagnated export, plummeted prices, production decline and other

unfavorable situation improved in varying degrees, industry profit margin also

appeared several months of recovery.

However, the situation of China's chemical fertilizer oversupply further

developed, and the situation in policy environment, production and logistics

costs and raw material supply remains rather grim, coupled with the impact of a

prolonged slump in international prices, domestic fertilizer market in the

second half backed into the bottom. Prices of various fertilizers had a

substantial decline. The industry profit margin is comprehensively lower than

that of last year, the loss-making percentage close to the five-year highs.

BOABC expected that favorable factors that affect 2010 fertilizer market

include: macro-economic policies will continue to take stimulating economic

growth and expansion of domestic market as the main objective (although its

intensity may be reduced); government continues to increase agricultural

investment and subsidies, especially agricultural material subsidies directly

for farmers to purchase fertilizers is expected to increase year by year, and

the linkage mechanism with fertilizer prices is established; grain purchase

price is also increasing steadily; Year 2009 is the 7th consecutive year of

grain harvest, which is conducive to supporting the growth of fertilizer

consumption; investment policies in fertilizer circulation has basically

liberalized; low export tariff policy in 2010 will continue to be implemented,

and so on.

Negative factors include: domestic and international economic situation are

still in recovery phase, the capacity of fertilizer consumption growth is

limited; it is not only difficult to alleviate the current situation of

fertilizer oversupply, but also the situation will be intensified in 2010;

production, logistics, environmental protection and other costs are still on the

rise; dependence on potash, sulfur and other raw materials are still high;

preferential policies on fertilizer industries would be phased out, and so on.

China's sulfuric acid price to hit new high after Chinese New Year

January 21, 2010 - The factory price of concentrated sulfuric acid in

China is expected to reach a new high after the Chinese New Year after

increasing to RMB 450 per ton recently from RMB 150 per ton in October 2009,

sources reported. The price surge

mainly resulted from the rising cost and growing demand, said industry analysts,

adding that the demand may grow significantly after the Spring Festival when the

farmers started plant crops.

Reportedly, 75% to 80% of sulfuric acid is used in the production of fertilizers

in China. Statistics show that

China's phosphate fertilizer capacity is 20 million tons at present.

Higher Sulfuric Acid

Prices To Help Chinese Copper Smelters

January 20, 2010

- Chinese copper smelters may be able to offset some of the revenue losses from

lower treatment and refining charges settled with global miners this year thanks

to higher sulfuric acid prices in domestic markets. Smelters have reached

2010 copper treatment and refining charges, or TC/RCs, with BHP Billiton Ltd.

and U.S.-based Freeport McMoRan Copper & Gold Inc. at $46.50 a metric ton and

4.65 cents a pound, 38% lower than last year, a consequence of too much capacity

being brought online and an overreliance on imported concentrate supply.

The settled TC/RCs will make it hard for the struggling smelters to generate

revenues, given average production costs for copper refining of around $70/ton

and 7 cents a pound. "No doubt smelters won't make any money out of

this year's refining fees, but normally they have other ways to make up for it,

such as sulfuric acid sales, increasing self-sufficiency in concentrate supply,"

said Che Hongyun, a senior metals analyst with Galaxy Securities Futures.

Sulfuric acid is a byproduct of copper cathode--refining a ton of cathode yields

three tons of sulfuric acid. Since the start of the year, the sulfuric

acid price has doubled from the average in 2009 to CNY400 a metric ton, high

enough for copper smelters to squeeze some profits from their refining

activities, industry participants said. "The current sulfuric acid price

certainly benefits copper smelters because demand from fertilizer makers keeps

it on a strong note these days," said Qiao Bo, an analyst with Beijing Antaike,

the state-owned metals consultancy. However, it is hard to store

sulfuric acid and the logistics costs are relatively high, so sales may still

bring in only a thin stream of revenue. Given still-sluggish demand for

fertilizer in overseas markets, "I don't see sulfuric acid prices going as high

as the historic level of around CNY1,800/ton in 2008...but the firmer price will

definitely help copper smelters make some money," said Antaike's Qiao.

A senior official from Tongling Nonferrous Metals Group (000630.SZ) said that

the company doesn't count on sulfuric acid sales: "We just need to make sure

that our sulfuric acid has places to go." "I think ultimately copper

smelters may rely on higher copper prices to secure profits," said He Xiaohui, a

copper analyst with Beijing Antaike.

The Future of Global Sulfuric Acid to

Depend on World Fertilizer Sector According to the Latest Research by Merchant

Research & Consulting, Ltd.

December 21, 2009 - LONDON – Demand for

sulfuric acid is mainly determined by the world

fertilizer sector. The latter has experienced the influence of deteriorating

global economy situation resulting in markets going down in the second half of

2008 - the beginning of 2009.

Sulfuric acid: 2009 World Market Outlook and

Forecast Updated: 11/2009/ 288 Pages

China Sulfur Industry Report, 2009

December 17, 2009 - ResearchInChina, the vertical portal for Chinese

business intelligence, announces the release of a new report - China Sulfur

Industry Report, 2009. For more information, please contact us at

report@researchinchina.com or at 86-10-82600893. For details of this

report please visit

http://www.researchinchina.com/Htmls/Report/2009/5795.html.

Along with the development of energy industry, the global by-product sulfur

output will continue to increase, and not be limited by market demand. At

present, China sulfur is mainly produced from petroleum refining, natural gas

processing and coal chemical processing, of which petrochemical industry

generates the most by recycling, and enjoys strong growth.

According to the statistics, China consumed about 10 million tons of sulfur in

2006, while its output was only 1-2 million tons; the consumption in 2007 was

10.85 million tons. Affected by the financial crisis in 2008, the consumption

decreased sharply to 8.75 million tons. In 2009, its consumption restored,

and reached 9 million tons in Jan.-Sep., more than that of full year of 2008.

It is forecasted that the total consumption in 2010 will be about 13 million

tons.

China’s sulfur demand is mainly satisfied by import. In 2007, it imported sulfur

of 9.647 million tons, up 9.6% yr-on-yr, and accounted for 90% of total

consumption. In 2008, it imported 8.414 million tons, down 12.9% yr-on-yr

affected by the financial crisis. With the economic recovery in 2009, the import

increased greatly, and it imported 9.72 million tons in the first nine months

alone, up 46.8% than the same period of 2008.

Viewed from the current sulfur and sulfuric acid supply situation in China, it

still needs to rely on import. However, with the release of sulfur capacity in

China since 2009, the import reliance will be changed after 2010.

Domestic-made sulfur is mainly sourced from subsidiaries of China Petroleum &

Chemical Corporation and PetroChina Company Limited. According to statistics,

there were more than 40 sulfur producers in China petrochemical industry in

2006, and among which 8 had annual output of above 50,000 tons, the largest

one--Maoming PetroChemical’s output reached 150,000 tons.

In Oct. 2009, the new sulfur recycling facility of 100,000 tons/year, solvent

regeneration facility of 500 tons/hour and sulfur packaging facility of Maoming

Petrochemical were put into operation successfully. In the same month, its

sulfur products passed national certification, which made Maoming Petrochemical

the first enterprise that had food-grade sulfur production ability and

qualification.

In 2010, with the construction and exploitation of the largest sulfur production

base in China - Sichuan Dazhou Natural Gas Field, the sulfur output of China

will get to 4.5 million tons. Also with the operation of gas fields in Northeast

of Sichuan Province of CNPC and CPCC, the tense supply situation of sulfur will

be relieved.

December 17, 2009 -

Industries that use sulfuric acid—and that includes nearly all the major

manufacturing sectors—have suffered a body blow from the faltering economy. As a

result, demand for sulfuric acid has plummeted over the past year, sending

prices on a downward spiral. And while experts say those prices may inch upward

a bit in 2010 as the economy perks up, the volatility in sulfuric acid prices

that occurred in the 2008–2009 period is very unlikely to return.

By any standard, the price fluctuations in sulfuric acid in the past two years

were unprecedented. According to

Purchasingdata.com, spot prices of sulfuric acid zoomed up from about

$80/ton in the summer of 2007 to nearly $400/ton in the summer of 2008, and then

hurtled downward to just over $100/ton a year later (see chart). By comparison,

the acid has sold in the $50–$85/ton range for much of the past decade.

One impact of the sudden dive in sulfuric acid prices over the past year is that

many acid buyers got stuck with a lot of high-priced inventory. According to

Robert Boyd, an analyst at the chemical consulting firm PentaSul in Houston,

last year at this time, after sulfuric acid prices had reached record highs, the

expectation from both buyers and sellers was that this inflationary trend would

continue into 2009. So buyers settled for one-year sulfuric acid contracts at

prices they knew were very high by historical standards, but which they thought

would seem relatively low as 2009 progressed.

"In retrospect, those contract prices ended up looking relatively high," says

Boyd, as the economic slump caused sulfuric prices to drop dramatically

throughout 2009.

As buyers negotiate sulfuric contracts for 2010, Boyd says that prices agreed to

this time around will be substantially lower than those negotiated last year.

Suppliers, he explains, are willing to be flexible on pricing for 2010 contracts

because "the demand for acid is so weak."

At one Southern U.S. chemical company that buys large amounts of sulfuric acid,

the purchasing manager, who is negotiating new contracts for 2010, confirms that

sulfuric acid suppliers "are anxious to make a deal" at lower contract prices

than last year due to concerns about demand being soft in the coming year, even

though most forecasters predict a slight upturn in the market.

On the other hand, this buyer doesn't expect bargain-basement prices either. One

reason, says the buyer, is that metals smelters, which produce sulfuric acid as

a byproduct, have been hard hit by low metals prices, and are unwilling to

accept sulfuric rates that would hurt their bottom line.

Another sulfuric acid buyer, Mike Houser, purchasing agent at ADM Corn

Processing in Decatur, Ill., says that one of his two sulfuric suppliers has

dropped rates as market prices have come down, while the other is likely to do

the same soon.

One factor that could influence sulfuric acid rates in 2010 is the price of

sulfur, a sulfuric feedstock, which rocketed to a towering peak of more than

$600/ton at the port of Tampa in the third quarter of 2008 and then plunged to

near zero by early 2009. Sulfur is now rising modestly, with tags hovering

around $30/ton. But this slight upturn is not necessarily a harbinger of much

more expensive sulfuric, notes Boyd, even though some sulfuric acid prices are

indexed to sulfur. The reason, he says, is that the traditional price coupling

of the two commodities "has mostly gone away" since sulfur's steep fall last

year.

Meanwhile, the output of sulfuric in North America has been shrinking. U.S.

production of the acid in the first half of 2009 was some 24% less than in the

same period a year earlier, according to U.S. Dept. of Commerce data. In Eastern

Canada, a combination of strikes and shutdowns at metals smelters have reduced

the available amounts of byproduct sulfuric acid. Both situations "are likely to

be resolved, to some extent, by next year," Boyd comments. "So we anticipate

more supply."

Right now, the market for sulfuric is "balanced to slightly long," says Key

Compton, president of Southern States Chemical, a Savannah, Ga.-based supplier

of sulfuric acid. Despite the closure of the Canadian plants, he says the acid

"is still easy to get, both domestically and internationally." That situation is

unlikely to change over the next year, Compton adds. At ADM Corn Processing, a

unit of agribusiness giant Archer Daniels Midland, Houser reports few recent

problems obtaining sulfuric, except for last year "at the height of the

commodities bubble."

The demand picture for sulfuric is highly variable. "If you sell the acid and

are located in the Midwest, or are closely tied to the automotive or

construction industries, you've probably had a bad time," says Compton. On the

other hand, sulfuric markets in environmental and pollution control "haven't

fared so badly," he notes.

Overall, Compton estimates that demand for the acid in the Eastern U.S. was down

maybe 15–20% early this year over the same period in 2008. Demand has "improved

somewhat" since then, he says, so that for second half of 2009, it was down

perhaps 10–15% over the previous year.

Despite the lagging consumption, new investments in North American sulfuric acid

plants and equipment were up by 39% in 2009 over the previous year, reports

Industrial Info Resources, a Sugar Land, Texas-based consulting firm that tracks

plant outlays. However, Trey Hamblet, an analyst with the firm, says that

unexpected jump is due mostly to projects that were green-lighted before the

recession.

Looking ahead, sulfuric acid demand is likely to recover slowly along with the

rest of the economy, notes Kim Ross, market development director for NorFalco,

an Independence, Ohio-based merchant marketer of sulfuric acid. But that

recovery may come in fits and starts, he cautions, "with two steps forward and

one back."

Look for "modest increases" in sulfuric prices in 2010 as the recovery takes

hold, says Compton. "But I certainly don't expect to see the spikes in pricing

we saw in 2008."

Overall, sulfuric acid markets "will return to normal" in 2010, says Boyd, after

seismic shifts in the industry. Over the past year, he notes, "we had a very big

boom in sulfuric, then a big bust. Now we're coming out the other side of all

that." For sulfuric buyers, Boyd says it will mean prices "closer to historical

levels."

December 2, 2009 - In November, the Chinese price of sulfuric acid as a

whole experienced an upward trend. Now, 98% of sulfuric acid prices are 300

RMB/ton, increasing about 9.9% over October. The sulfuric acid market trends

differ between North and South China. The overall rise in price in the North

relies mainly on market pull, concentrated in Hebei, Tianjin and Shandong

provinces, where sulfuric acid prices are sharply rising.

North

Market Sulfuric Acid Price Rising

Hebei,

Tianjin and Shandong sulfuric acid manufacturers in the north have raised

sulfuric acid prices to the range of about 80-180 RMB. The reasons are:

1.

Shandong copper smelters, affected by higher international copper raw material

costs and the lower processing fees, have made sulfuric acid production

abnormal, and with the deployment of part of the smelter acid factory park

maintenance, this has led to tight market supply.

2. In

the international market, the impact of rising sulfur prices has caused

elevation of Chinese sulfur prices.

By the

end of November, the Chinese solid sulfur prices were 620 or so; in the short

term, sulfuric acid prices will remain high. Under various favorable factors,

the downstream market demand is relatively stable, northern areas sulfuric acid

prices remain high.

From the

current market situation, from fertilizer to storage, accounting for the export

tariff reduction and other favorable factors, the operating rate of Chinese

phosphate fertilizer business has improved; the north China sulfuric acid

situation is good, inventories are small, but the market outlook is more

optimistic. Himfr expects that this improvement will continue until the end of

December.

South

Market in Weakness

Compared

with the northern region's sulfuric acid market situation, the southern region's

sulfuric acid market is relatively weak. Sulfuric acid prices are in varying

degrees of decline; concentrated in the Zhejiang, Hunan and Hubei regions, the

decline range is about 50-100 RMB.

Sulfuric

acid (http://himfr.com/list-product-Agriculture-01000000-1.html

) prices drops in south area are because of a general increase in pre-load of

fertilizer production enterprises, which basically already met the Chinese

demand for fertilizer in autumn. Judging from the current market situation, in

Jiangsu and Hubei provinces, sulfuric acid prices appear to be rebounding. Himfr

expects that sulfuric acid market will basically remain stable.

Himfr

reports that for the Chinese fertilizer, pesticide and other industries in the

production preparation period, the raw material prices will rise slightly in

December. In the short term, the oversupply situation of sulfuric acid will not

change.